Snapshot: Interest Rate Hikes and Your Local Housing Market

Federal Reserve Interest Rate Hikes

The Federal Reserve interest rate hikes trying to tame high inflation have caused most asset classes to suffer double digit losses, including real-estate, stocks, bonds, and crypto. Even though mortgage rates are influenced by the 10-year treasury yield, and are not directly impacted by the FED rate hikes, these hikes do influence mortgage rates.

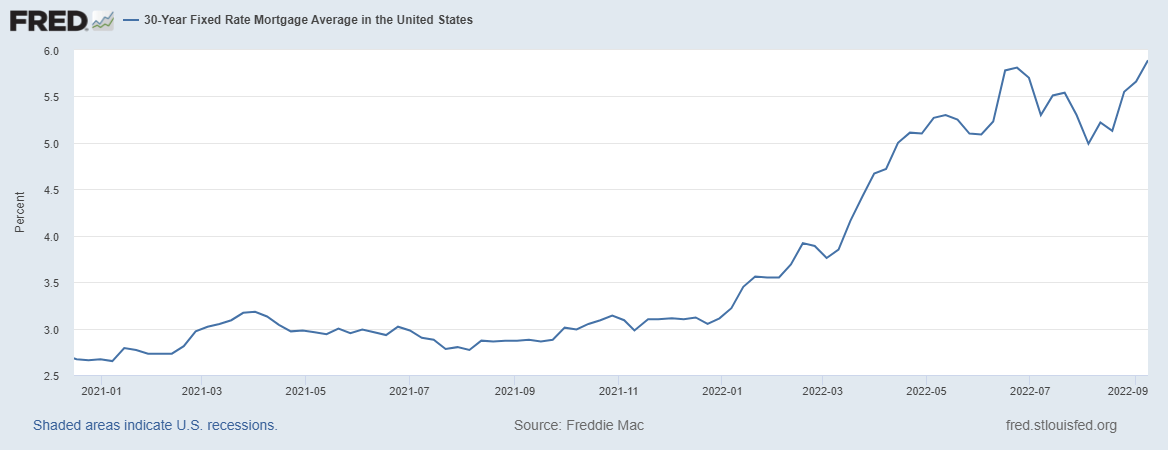

Mortgage lenders tend to price in future expectations of interest rate hikes by the FED, even before they are announced, therefore affecting your local housing market. The 30-year mortgage rate reached 5.5%, nearly doubling the rate from 12-months ago, and the housing market still does not reflect the higher mortgage rates.

Average 30-Year Fixed Rate Mortgage

Housing prices have been at peak levels throughout the pandemic due to the FED funds rate being near 0%. Now that the rates are higher, in theory that should mean that home prices should be lower. However that is not the case, interest rates surged in a matter of months and the housing market is playing catch up to cool down. Rents have surged alongside inflation, and the average consumers are being punished.

How Interest Rate hikes are Affecting Buyers and Sellers

As borrowing costs for businesses and consumers rise, the era of ‘cheap money’ through 2020-2021 has ended, and companies in the face of a recession are letting people go. Ford is laying off nearly 3,000 workers. High inflation, higher interest rates and job losses could cause a surge in home foreclosures and bankruptcies throughout the country.

Even half a percent point raise in mortgage rates could mean hundreds of dollars extra in mortgage payments, therefore hurting both buyers and sellers. Investors/sellers that were hoping to cash in on higher housing prices during the pandemic, may no longer be able to sell their properties due to less demand. However, fewer buyers could mean cheaper prices, and if timed right, purchasing real estate at cheap prices could prove very fruitful in the long run for investors. Keeping in mind that interest rates do tend to fluctuate over time, and even though the interest rates seem high now, they will eventually come down and a buyer will be able to refinance their remaining mortgage at a lower interest rate.

Currently though, this steady increase of mortgage rates in the last few months have affected different states (areas) across the US disproportionally. The wealthier parts of the country like New York’s Hudson Valley are yet to see any significant difference in people purchasing homes, while other parts of the country are seeing dramatic drops in mortgage applications as well as housing purchases.

Even though the Fed has some control over the housing market in the US, the pandemic has also pushed us into a historically unprecedented situation. With supply chain issues, manufacturing shortages, and unemployment, there are simply too many variables affecting the housing market. Furthermore, builder sentiment regarding the uncertainty of the market is also a key factor.

Builders do not know how or when the rates will start coming down and sales will start going back up again. Therefore, many builders are now stuck with previously unsold inventory and are withholding any future building prospects.

What You Should Consider Before Purchasing a Home

Understanding interest rates and current housing market conditions could affect your financial health in a variety of ways.

If your interest rate is high then you are paying your lender more on top of the principal amount, to lend you the money for your purchase. Generally you should be looking for fixed-interest rates so that you know exactly what you will be paying for the duration of your mortgage. Recently interest rates have been very volatile because the Federal Reserve raised the Federal Funds Rate to discourage borrowing and slow consumer demand, since lower interest rates increase demand, drive up prices and inflation. Right now the main goal of the FED is to tame down inflation.

However, after interest rates have significantly increased an economy may enter into a recession. There's four stages in an economic cycle: peak, recession, trough, and expansion. During the recession or trough stages could be excellent times to make real estate purchases since historically, that's when interest rates start coming down to enter the expansionary period, causing asset prices to start going up eventually towards their peak.

Bottom Line

Every geographical area and its local housing markets are reacting differently to the FED raising interest rates. Understanding for yourself what may be a good time to make a home purchase where you live, at a good price and interest rate is absolutely essential for your financial health.

The Local Economist

Your Home for Entrepreneurial News, Local Business Spotlights, and Trends that Matter

join the newsletter

Recent Posts

Share This...